In an earlier blog I showed that after the financial crisis of 2007-08 real wages fell, while the amount of output produced by each hour worked in the economy rose at a far lower pace than earlier. Figure 1 below reproduces the data from that earlier blog.

Figure

1 The collapse of productivity growth in

the UK economy post the financial crisis

In this blog I want to answer the

question as to why that output per hour worked grew so much slower than before

the financial crisis. Why was this crisis so very different from earlier

recessions?

Teresa May, during the 2017 general

election campaign, said there was ‘no magic money tree’ when asked by a nurse

why her pay had been frozen. Well, was

that true? A ‘magic money tree’ is an informal way of describing what has been

happening to now rich countries for the last 200 years in that the amount of

output each produces grows faster than does the labour to produce that output. Her

more accurate answer, as the above figure shows, should have been that under

previous governments there had been a ‘magic money tree’ but that the

conservative dominated governments after 2010 had succeeded in killing it

off. This blog is about the mechanisms

by which death was affected.

If you work hard and do your job,

what if each year you produced more with no additional effort on your part. It

sounds a bit unlikely but that is exactly what the UK economy did up to the

financial crash. Economists call it total factor productivity (TFP). It is,

quite literally, a measure of how much more output you get without more inputs

into production (or at least any that are measurable).

Figure 2 More output but not more inputs

Source ONS data: Release

of Productivity Overview, UK: October to December 2021. The figure for TFP in

the chart is for the Total Market Sector.

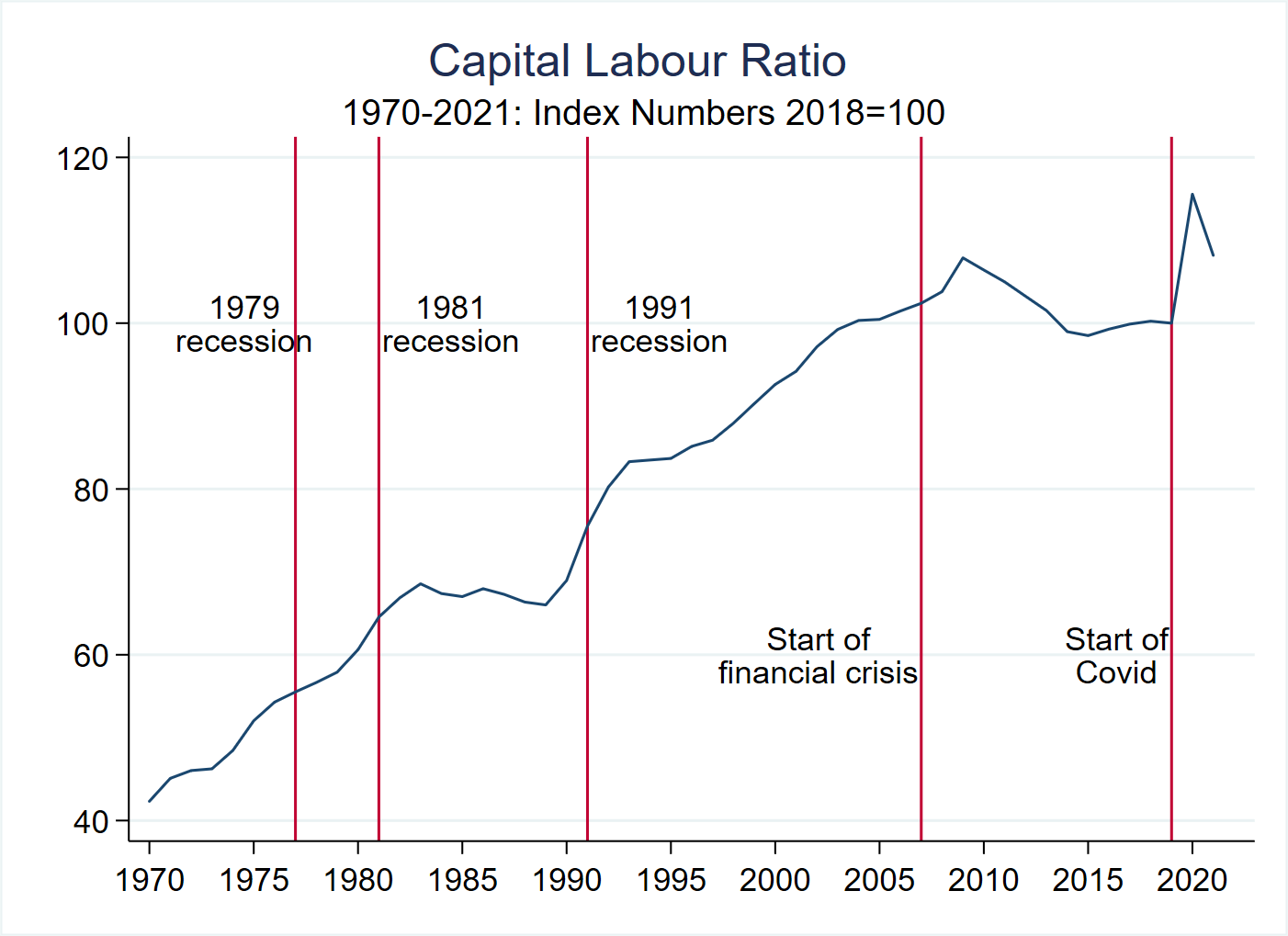

Figure

3 How much more capital did workers have?

Figure 4 Changes in capital and labour inputs

Source ONS data: Release of Productivity Overview, UK: October to December 2021. Capital services and labour hours are for the Total Market Sector.

While we can see from Figure 3 that

the amount of capital each worker has to work with fell soon after the

Financial Crisis, we need to know how this changed occurred and that we show in

Figure 4.

Two changes occurred after the

financial crisis which were quite different from earlier recessions. The first

was that capital services grew much more slowly than before. The second was

that, in dramatic contrast to earlier recessions, labour supply started to grow.

The result was the decline in the capital to labour ratio.

We can now answer the question we

posed in the title to this blog as to why labour productivity growth collapsed

after the Financial Crisis. Labour productivity growth depends on two factors.

The first is TFP (Total Factor Productivity) which is the magical factor producing

more output with no more inputs. While this fell marked immediately following

the crisis it then started to rise again. The second factor is the capital to

labour ratio which we showed in Figure 3 fell significantly after the financial

crisis. It is this fall which is the most important factor explaining the

failure of labour productivity to rise by more than very modest amounts.

Labour productivity is not the focus

of political debate. Indeed, outside the columns of relatively specialised

newspapers it is not mentioned at all. That is regrettable as it is the

collapse of that growth in labour productivity that underlies all the UK’s

present economic woes. It explains the low wages many workers face, it explains

the inability of the government to fund adequately the NHS and social care, it

explains why at the end of a decade of ‘austerity’ there was still no budget

surplus and the advent of the pandemic ensured that to address it the result

has been a public sector deficit far larger than when ‘austerity’ began. It

drives real earnings. It is how all of the painful political choices can be

avoided. As real incomes rise taxes will rise even if tax rates do not change,

there will be more income for workers and more funds for public services.

Put simply more people in the UK

have been working so output has been rising but the amount of output each

produce has not been increasing – the end of the magic money tree. This shows

up in Figure 5 below where, following the financial crisis, after a short term

fall, output continued to grow while output per person did not. As Figure 5

also shows this had not happened after any earlier recessions.

Figure

5 How output grew and productivity did not after the financial Crisis

Sources: As for Figure 1.

While the above analysis shows how the decline in productivity has been affected, the results clearly poses two more fundamental questions. Why did labour supply start rising and investment start falling after the recession caused by the Financial Crisis, while neither had happened in earlier recessions? To that I will return in a future post.

No comments:

Post a Comment